19 Jul 2023

Since the beginning of 2021, the proportion of countries whose net zero targets are set in legislation or policy documents has grown from single digits to 75%.

Companies face new opportunities and risks related to their impact on greenhouse gas emissions.

Technological innovations will be vital to achieve net zero goals, creating compelling opportunities for long-term investors.

Learning About ESG is an educational series that connects environmental, social and governance topics with investing.

Join us each issue to see how global developments can have implications for investors. The better we understand ESG, the bigger the role it can play in our everyday lives – and investment portfolios – contributing to a better world.

‘Net zero’ is achieved when greenhouse gases are no longer added to the atmosphere. This doesn’t require us to completely eliminate activities that generate greenhouse gases, but means solutions to offset unavoidable emissions, by reducing the amount left in the atmosphere, result in a net amount of zero added.

Last month was the hottest June ever recorded on the planet, according to the World Meteorological Organisation. Sadly, heat records nowadays tend to be short-lived. Over four consecutive days in the first week of July, the planet experienced its hottest days in modern history.

After over a century of filling the atmosphere with greenhouse gases, mankind has already caused over 1°C of global warming. The impact goes beyond higher temperatures, also causing more extreme weather events such as heatwaves, storms and droughts. This affects everyone as it impacts our basic survival needs.

Unchecked climate change will damage our ability to grow crops, further strain water supplies and necessitate mass migration as areas become uninhabitable due to lack of water, arid land and other factors. More frequent extreme weather events add to the issue - in 2021, weather-related disasters displaced 45 million people1. There’s a long list of financial implications. One already felt by all is food inflation impacted by crop failures.

The UN estimates that 3.5 billion people, nearly half of the world’s population, live in areas highly vulnerable to climate change impacts. This is clearly a global issue of urgency. Positively, governments are rapidly enacting new laws and regulations to drive the transition to net zero, which includes incentivising clean energy investments.

Since the beginning of 2021, the proportion of countries whose net zero targets are set in legislation or policy documents has grown from single digits to 75%. Likewise, of the world’s largest 2,000 companies, those with net zero targets now represent two-thirds of total annual revenue2.

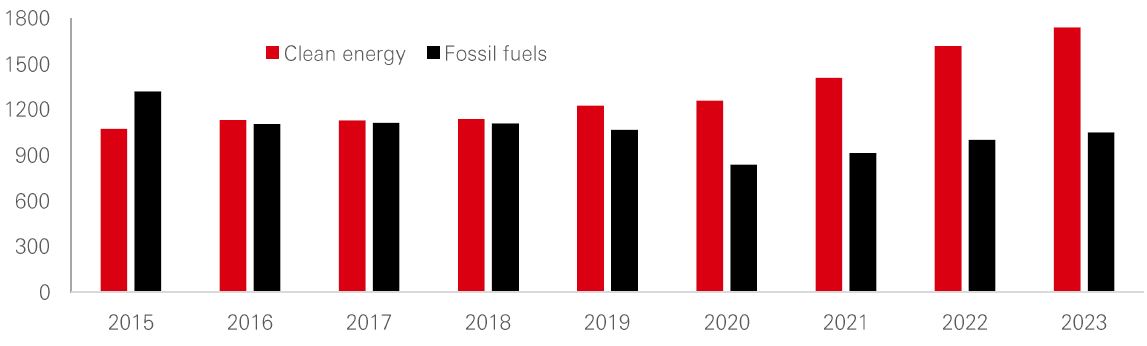

Source: International Energy Agency, May 2023. Figure for 2023 is projected.

Effective management of climate change hinges on swift and large-scale global action. The realisation of risks to populations and economies has resulted in governments now taking steps to oblige. This means companies face new opportunities and risks related to their impact on greenhouse gas emissions.

According to UN projections, limiting global warming to 1.5°C requires greenhouse gas emissions to peak no later than 2025. Countries that have announced, pledged, or adopted climate plans to reduce emissions account for over 90% of global output and around 88% of global carbon emissions3. Yet, these plans and commitments must go further to reverse the current emissions trajectory at a fast enough pace.

Momentum is gathering, as evidenced by last year’s US legislation to accelerate its transition to net zero, with subsidies to boost investment in clean technology across industries. Funding is estimated to amount to USD500 billion over the next decade.

Not to be outdone, Europe has built on its own net zero transition plans, enacting new policies to decarbonise economies across the region. State aid will amount to up to USD110 billion per year to 2027 in support of the development of clean technologies.

Separately, various carbon pricing schemes have been implemented across most of the largest economies, essentially adding a cost to the operations of heavy greenhouse gas emitters. Both sides of these policy actions clearly incentivise companies to pursue decarbonisation solutions.

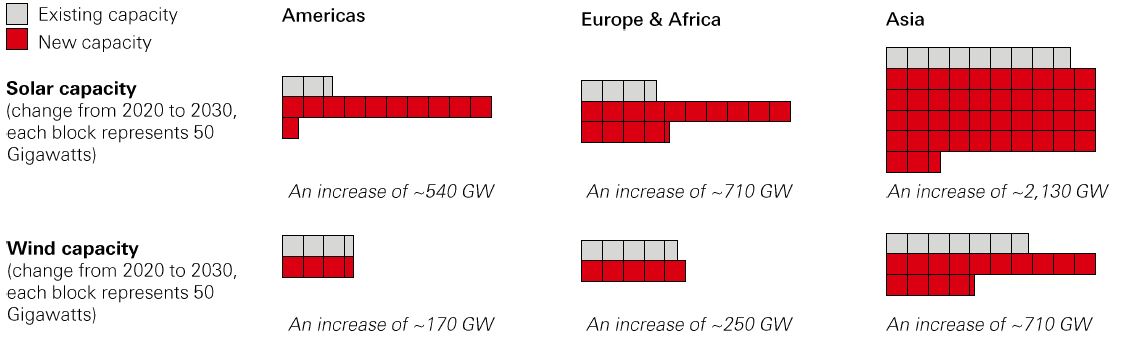

The chart below provides scale for the change underway to transition economies towards net zero, with no opportunity bigger than in Asia where there’re more individual policies in force to incentivise the use of renewables than in any other region. Clean energy investment in China has grown by a third in the last three years alone, reaching more than USD500 billion last year4.

Source: Bloomberg NEF, HSBC Asset Management, February 2023.

Economies must be redesigned if we’re to avoid the most dire consequences of climate change. Innovation is the answer and presents opportunities for long-term investors.

The technological innovation of the industrial revolution set us on the path towards a climate crisis, and technological innovation is now needed to avert it. Solutions extend beyond implementing renewable energy.

For instance, more energy generated by renewables requires storage. This creates opportunities for battery storage solutions, and hydrogen as an alternative energy store which releases only steam as a by-product when producing power. Hydrogen-powered trains have already been rolled out in Germany and China, and should arrive in India by the end of the year.

Transportation contributes roughly a quarter of greenhouse gas emissions globally, making it a vital industry for decarbonisation. The transition to electric vehicles is key to this, making recent developments in technologies such as sodium-based batteries important. Reliance on today’s lithium-based batteries may not be feasible given that demand for lithium is projected to increase 26-fold in the 2030s, potentially outpacing supply.

Examples extend across industries, from capabilities to capture carbon released in industrial processes, to incorporating new approaches and technologies in farming that reduce emissions, and changes in how we build and use products to reduce material waste and the energy-intensive process of extracting more from the ground.

For investors there’re multiple ways to pursue the opportunity. Prioritising exposure to companies with a smaller carbon footprint is a logical approach. Another is specifically targeting exposure to leaders of the change being undertaken to transition to net zero.

Asset managers can go beyond designing portfolios focused on the net zero transition. Managing large pools of capital creates leverage for engaging with companies to accelerate their transition. HSBC is part of the Net Zero Asset Managers initiative tackling this, with roughly USD60 trillion in assets cumulatively. We’re also one of the first signatories to the Principles for Responsible Investment, back in 2006.

ESG: a set of Environmental, Social and Governance criteria that investors can apply to analyse and identify material risks and growth opportunities in investments.

Carbon emissions: are emissions stemming from the burning of fossil fuels during any kind of manufacturing process.

Climate change: the change in the planet’s climate and weather due to the release of greenhouse gases into the atmosphere.

Greenhouse gases: gases that create a greenhouse effect and warming of the planet, with carbon dioxide being the most common.

Recent US and EU policy initiatives highlight the importance of battery technology...[22 Sep]

Biodiversity is crucial for human survival, providing essential resources and ecosystem...[4 May]

Climate change poses a significant threat to coffee production as suitable land for...[13 Oct]

ESG practices can impact a company’s prospects and value, with ESG leaders broadly...[4 Jul]

Important information for Customers

WARNING: THE CONTENTS OF THIS DOCUMENT HAVE NOT BEEN REVIEWED BY ANY REGULATORY AUTHORITY IN SINGAPORE OR ANY OTHER JURISDICTION. YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE INVESTMENT AND THIS DOCUMENT. IF YOU ARE IN DOUBT ABOUT ANY OF THE CONTENTS OF THIS DOCUMENT, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

This document has been issued by HSBC Bank (Singapore) Limited (the "Bank") in the conduct of its business in Singapore and may be distributed in other jurisdictions where its distribution is lawful. It is not intended for anyone other than the recipient. The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document must not be distributed to the United States, Canada or Australia or to any other jurisdiction where its distribution is unlawful. All non-authorized reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings.

This document has no contractual value and is not and should not be construed as an offer or the solicitation of an offer or a recommendation for the purchase or sale of any investment [in any jurisdiction in which such an offer is not lawful] or subscribe for, or to participate in, any services. The Bank is not recommending or soliciting any action based on it.

The information stated and/or opinion(s) expressed in this document are provided by HSBC Global Asset Management (Singapore) Limited. We do not undertake any obligation to issue any further publications to you or update the contents of this document and such contents are subject to changes at any time without notice. They are expressed solely as general market information and/or commentary for general information purposes only and do not constitute investment advice or recommendation to buy or sell investments or guarantee of returns. The Bank has not been involved in the preparation of such information and opinion. The Bank makes no guarantee, representation or warranty and accepts no responsibility for the accuracy and/or completeness of the information and/or opinions contained in this document, including any third party information obtained from sources it believes to be reliable but which has not been independently verified. In no event will the Bank or HSBC Group be liable for any damages, losses or liabilities including without limitation, direct or indirect, special, incidental, consequential damages, losses or liabilities, in connection with your use of this document or your reliance on or use or inability to use the information contained in this document.

In case you have individual portfolios managed by HSBC Global Asset Management Limited, the views expressed in this document may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management Limited primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

The information contained within this document has not been reviewed in the light of your personal circumstances. Please note that this information is neither intended to aid in decision making for legal, financial or other consulting questions, nor should it be the basis of any investment or other decisions. You should carefully consider whether any investment views and investment products are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. The investment decision is yours but you should not invest in any product unless the intermediary who sells it to you has explained to you that the product is suitable for you having regard to your financial situation, investment experience and investment objectives. The relevant product offering documents should be read for further details.

Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Such statements do not represent any one investment and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We can give no assurance that those expectations reflected in those forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. We do not undertake any obligation to update the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investment involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Past performance information may be out of date. For up-to-date information, please contact your Relationship Manager.

Investment in any market may be extremely volatile and subject to sudden fluctuations of varying magnitude due to a wide range of direct and indirect influences. Such characteristics can lead to considerable losses being incurred by those exposed to such markets. If an investment is withdrawn or terminated early, it may not return the full amount invested. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in certain jurisdictions. Narrowly focused investments and smaller companies typically exhibit higher volatility. There is no guarantee of positive trading performance. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks. You should read all scheme related documents carefully.

© Copyright. HSBC Bank (Singapore) Limited (Company Registration No. 201420624K). All rights reserved.

Notes

1. The Internal Displacement Monitoring Centre (IDMC) ) 2021 Global Report on Internal Displacement.

2. Net Zero Stocktake, June 2023: New Climate Institute, Oxford Net Zero, Energy & Climate Intelligence Unit and Data-Driven EnviroLab.

3. UN Climate Action Tracker; McKinsey Energy Insights Global Energy Perspective 2022.

4. International Energy Agency, Energy investment in China, 2019 and 2022.