Learning about ESG: Progressing ESG adoption in Asia

4 Dec 2023

Travis Tucker, CFA

HSBC Asset Management Research & Insights Senior Manager

Geoffrey Lunt

HSBC Asset Management, Head of Asia Investment Specialists

The scarcity of ESG investment products and fragmented data across the region have hindered widespread adoption of ESG principles in Asia.

However, there’s a positive shift taking place as the region moves towards implementing ESG disclosure and transparency requirements.

This development should only make the region more appealing to global investors pursuing the opportunity of higher yields amidst stable and deepening credit markets.

Learning About ESG is an educational series that connects environmental, social and governance topics with investing.

Join us each issue to see how global developments can have implications for investors. The better we understand ESG, the bigger the role it can play in our everyday lives – and investment portfolios – contributing to a better world.

While awareness and adoption are on the rise, up to now Asia hasn’t displayed the same degree of regulatory emphasis on ESG integration as Europe, and to a lesser extent, the US.

The scarcity of available ESG investment products in the region acts as a deterrent to a broader audience of investors, limiting their ability to invest in line with sustainable principles. The fragmentation of ESG data and disclosure practices across Asia further compounds the challenges, with a clear distinction between developed and emerging markets in the region. In particular, financial hubs like Singapore and Hong Kong are making strides toward aligning with European regulatory and corporate disclosure standards.

The absence of consistent company disclosures in emerging Asia poses a significant hurdle to ESG adoption. Due to a lack of standardised rules across countries, inconsistencies impede investors' ability to assess ESG factors. In this context, regulators in Asia have a crucial role to play in introducing consistent policies.

Asia faces diverse yet significant sustainability-related risks. For instance, the region is highly vulnerable to physical risks induced by climate change. However, much of developing Asia currently prioritises economic growth heavily reliant on natural resources and carbon-intensive industries, such as manufacturing – primarily due to outsourcing from developed markets. This results in a continually expanding carbon footprint that hinders their transition to a low-carbon economy, as shown in the chart below.

There’s a clear need to drive sustainable economic development over the long term, supporting the expectation for greater adoption of ESG practices and disclosure in the coming years.

Despite the substantial challenges faced in Asia, there are two main reasons for optimism: a growing demand for responsible investment opportunities and increasing regulatory support. This is evidenced by a twofold increase in the number of ESG policies from 2016 to 2021.1

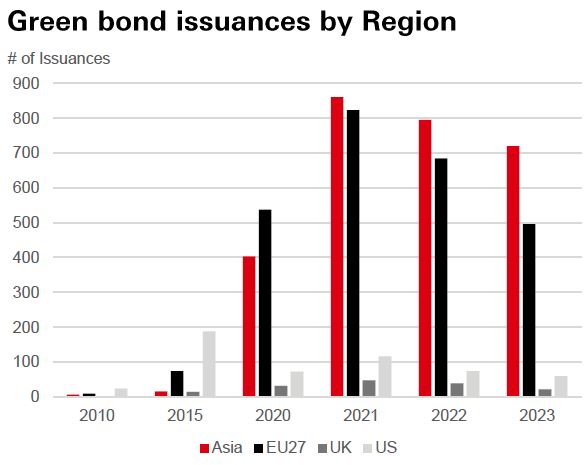

Significant progress has been made. For instance, Asia crossed the USD1 trillion milestone in the impact bond market in Q2 2023, accounting for roughly a quarter of global cumulative issuance of green, social, and sustainability-linked bonds.²

Importantly, bond markets offer more direct influence over the allocation of capital, compared to equity markets where investors are trading secondary securities. This, coupled with the massive need for funding of sustainable projects, has contributed to the remarkable growth of the sustainable bond market. Following a decline in issuance since the beginning of 2022, owing to rising interest rates and heightened market volatility, the market in Asia exhibited a robust recovery in the first half of this year.

While green bonds continue to dominate, comprising around 66% of bonds focused on ESG priorities, there has been a notable surge in social and sustainability bonds as well.3 The scale of funding required for Asia’s transition to a net zero economy, estimated at around USD30 trillion by 2050, supports expectations for significant growth ahead in sustainable bond issuance.

Beyond the expansion of sustainable bonds, the growth in ESG products in Asia is being catalysed by emerging ESG-fund labelling requirements. These requirements mandate that asset managers disclose how ESG factors are integrated into the investment process. Tighter regulations for corporate-level ESG disclosures and product-level transparency can greatly enhance corporate governance and market stability, while providing investors with better information to mitigate risks. In fact, companies in Asia that are aligned with the EU taxonomy have expanded their sector relative price premiums to 55% versus earnings, surpassing the global average of 37%.4 Moreover, there has been increasing support in Asia for disclosures recommended by the Task Force on Climate Related Financial Disclosures, with almost half of 3,400 global supporters being Asian organisations.5

In fast-growing India, whose development is increasingly attracting international investors, the Securities and Exchange Board has mandated Business Responsibility and Sustainability Reporting (BRSR) for listed companies to disclose ESG risks. These steps are clear indications of the progress being made in ESG disclosure and transparency in the region.

In 2023, India forayed into the sovereign green bond market, initiating two substantial USD1 billion local currency deals with plans for an additional USD2.2 billion equivalent issuance, aimed at mobilising resources for green infrastructure.

Proceeds of these sovereign green bonds are channelled towards investments in two critical areas: renewable energy and the electrification of transportation systems. These sectors are of immense significance, accounting for approximately 41% of India's greenhouse gas emissions in 2019 and projected to contribute two-thirds of emissions by 2050.6 This signifies the rising importance of green bond issuances in India and elsewhere, and their direct impact on long-term sustainability.

Such notable developments are occurring alongside growing attention on India's extensive USD1 trillion government debt market, following its inclusion in J.P. Morgan's benchmark emerging markets government bond indices. This inclusion will deepen the sovereign bond market in India, with a substantial influx of foreign capital estimated at around USD25 billion, and setting the stage for a ramping up of bond issuance to fund future development.

On a broader scale, the deepening bond markets in Asia bode well for addressing long-term sustainability goals. Private capital will play a significant role in both economic development and the region’s energy transition. Alignment with international standards, improved governance and enhanced disclosure practices will encourage capital flows that support sustainable development.

Given the benefits of ESG integration within Asia – notably, improved investment decisions as a result of better transparency and risk mitigation – ESG disclosure progress should only make the region more appealing to global investors pursuing the opportunity of higher yields amidst stable and deepening credit markets. Professional asset managers can assist through investment processes that integrate ESG considerations. This includes assessing ESG risks, carrying out enhanced due diligence of higher risk issuers and actively engaging with companies to address risks and achieve positive outcomes.

ESG: A set of Environmental, Social and Governance criteria that investors can apply to analyse and identify material risks and growth opportunities in investments.

EU Taxonomy: Classification system that defines criteria for economic activities that are aligned with a net zero trajectory by 2050 and the bloc’s broader environmental goals.

Sustainable Bonds: Used to finance or re-finance a combination of green and social projects or activities.

Share

Related insights

Recent US and EU policy initiatives highlight the importance of battery technology...[22 Sep]

Since the beginning of 2021, the proportion of countries whose net zero targets are...[19 Jul]

Biodiversity is crucial for human survival, providing essential resources and ecosystem...[4 May]

Climate change poses a significant threat to coffee production as suitable land for...[13 Oct]

Important information for Customers

WARNING: THE CONTENTS OF THIS DOCUMENT HAVE NOT BEEN REVIEWED BY ANY REGULATORY AUTHORITY IN SINGAPORE OR ANY OTHER JURISDICTION. YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE INVESTMENT AND THIS DOCUMENT. IF YOU ARE IN DOUBT ABOUT ANY OF THE CONTENTS OF THIS DOCUMENT, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

This document has been issued by HSBC Bank (Singapore) Limited (the "Bank") in the conduct of its business in Singapore and may be distributed in other jurisdictions where its distribution is lawful. It is not intended for anyone other than the recipient. The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document must not be distributed to the United States, Canada or Australia or to any other jurisdiction where its distribution is unlawful. All non-authorized reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings.

This document has no contractual value and is not and should not be construed as an offer or the solicitation of an offer or a recommendation for the purchase or sale of any investment [in any jurisdiction in which such an offer is not lawful] or subscribe for, or to participate in, any services. The Bank is not recommending or soliciting any action based on it.

The information stated and/or opinion(s) expressed in this document are provided by HSBC Global Asset Management (Singapore) Limited. We do not undertake any obligation to issue any further publications to you or update the contents of this document and such contents are subject to changes at any time without notice. They are expressed solely as general market information and/or commentary for general information purposes only and do not constitute investment advice or recommendation to buy or sell investments or guarantee of returns. The Bank has not been involved in the preparation of such information and opinion. The Bank makes no guarantee, representation or warranty and accepts no responsibility for the accuracy and/or completeness of the information and/or opinions contained in this document, including any third party information obtained from sources it believes to be reliable but which has not been independently verified. In no event will the Bank or HSBC Group be liable for any damages, losses or liabilities including without limitation, direct or indirect, special, incidental, consequential damages, losses or liabilities, in connection with your use of this document or your reliance on or use or inability to use the information contained in this document.

In case you have individual portfolios managed by HSBC Global Asset Management Limited, the views expressed in this document may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management Limited primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

The information contained within this document has not been reviewed in the light of your personal circumstances. Please note that this information is neither intended to aid in decision making for legal, financial or other consulting questions, nor should it be the basis of any investment or other decisions. You should carefully consider whether any investment views and investment products are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. The investment decision is yours but you should not invest in any product unless the intermediary who sells it to you has explained to you that the product is suitable for you having regard to your financial situation, investment experience and investment objectives. The relevant product offering documents should be read for further details.

Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Such statements do not represent any one investment and are used for illustration purpose only. Customers are reminded that there can be no assurance that economic conditions described herein will remain in the future. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We can give no assurance that those expectations reflected in those forward-looking statements will prove to have been correct or come to fruition, and you are cautioned not to place undue reliance on such statements. We do not undertake any obligation to update the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

Investment involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless and investors may not get back the amount originally invested. Past performance contained in this document is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Past performance information may be out of date. For up-to-date information, please contact your Relationship Manager.

Investment in any market may be extremely volatile and subject to sudden fluctuations of varying magnitude due to a wide range of direct and indirect influences. Such characteristics can lead to considerable losses being incurred by those exposed to such markets. If an investment is withdrawn or terminated early, it may not return the full amount invested. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavourable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in certain jurisdictions. Narrowly focused investments and smaller companies typically exhibit higher volatility. There is no guarantee of positive trading performance. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Mutual fund investments are subject to market risks. You should read all scheme related documents carefully.

© Copyright. HSBC Bank (Singapore) Limited (Company Registration No. 201420624K). All rights reserved.

Notes

1.Goldman Sachs Global Investment Research, February 2022.

2.OECD, September 2023.

3.LSEG, August 2023.

4.Goldman Sachs Global Investment Research, February 2022.

5.PwC, September 2022.

6.World Bank, June 2023.